Reflections on “The Number” by David D. Kirkpatrick - The New Yorker.

The FIRE sector in all its unproductive detail, hopeless and appalling.

I recently rote an essay about Trump crypto. Here we have the entire Trump shebang extending into the non-productive all American nightmare of now.

‘Trump had boasted constantly, and in detail, about how rich he was. “He doesn’t talk about it anymore,” Wertheimer said. “He may be the greatest con artist in American history.”

Reflections on “The Number” by David D. Kirkpatrick

This evening I dove into David Kirkpatrick’s mammoth New Yorker investigation—the piece is titled “The Number,” and it examines just how much Donald Trump and his family have actually profited from his time in the White House.

At first I thought I was simply reading an eye-opening financial profile of Trump. By the end, I realized I had encountered something far deeper: an unflinching indictment of the entire American economic system, where the FIRE sector—finance, insurance, and real estate—rules supreme.

But what really struck me wasn’t just the sheer size of Trump’s haul. It was how this case study illuminated a broader truth: our economy increasingly rewards deal-makers, lobbyists, and speculators—people who move money and influence around—while devaluing anyone who actually builds things, writes books, teaches students, designs homes, or creates beauty. There are no Frank Lloyd Wright’s, Aaron Copeland’s or Henry Ford’s mentioned anywhere here.

My First Impressions

When I reached the article’s staggering figure—roughly $3.4 billion in profits tied directly to Trump’s presidency—I paused. It’s one thing to hear headlines about “pay-to-play”; it’s quite another to see how those headlines add up to billions in real dollars. From Saudi investments and exclusive club fees to crypto ventures and Gulf-state private jets, the revelations kept coming.

The Parasitic FIRE Economy

Kirkpatrick’s reporting dovetails with decades of scholarship showing that finance has ballooned from about 10 percent of GDP in 1950 to more than 20 percent today, even as manufacturing and R&D have stalled. Wall Street now generates around 40 percent of corporate profits while employing barely 5 percent of the workforce. We’ve shifted from an economy that once channeled capital into factories, farms, and innovation to one that profits from moving money around itself.

Reading about Trump’s deals—cabinet officials flying his planes, foreign governments bankrolling his businesses—felt like watching a vivid, real-time exhibit of financialization at its most naked: rent-seeking masquerading as entrepreneurship.

Meetings Over Production

One of the most revealing patterns in the article is the piling up of meetings, dinners, and ribbon-cuttings that generate fees and favors but no tangible product. It reminds me of a carnival mirror held up to our elite class: endless photo-ops and negotiations, but no factories humming, no new ideas being prototyped, no poems being published—just transactions.

If you believe that the purpose of economic life is to create, to write, to build, to compose, then what Kirkpatrick exposes is profoundly alien. The world he describes is about proximity to power, not contribution to culture or civilization. It’s an economy of smoke and mirrors, where wealth accrues to those best at weaving webs of influence.

Why This Matters

I’ve long worried about the moral bankruptcy of rent-seeking capitalism, but “The Number” made it visceral. It’s one thing to read academic studies on financialization; it’s another to see how that process enabled a former reality-TV star to monetize the presidency itself. And if the president can do it, why not everyone with connections—and enough chutzpah to turn public office into a private cash machine?

That realization is why I came away convinced this article isn’t just about Trump. It’s about an economy that rewards extraction over creation. An economy that, as Kirkpatrick unwittingly shows, can survive only by hollowing out its productive core and substituting influence and rent-capture for genuine value.

Over to You

I’d love to hear your thoughts. Did Kirkpatrick’s number shock you? Do you see the same disconnect between finance and production in your own work or community? And, most importantly, does this feel like a system that can—or should—be reformed, or is it beyond repair? Let me know in the comments

The New Yorker is behind a paywall. I subscribe. I imagine you will be able to access part of the lengthy essay.

Here’s the link to David D. Kirkpatrick’s article in The New Yorker:

https://www.newyorker.com/magazine/2025/08/18/the-number

I don't know if this will paste but I attempt to paste the article here. Read on, if you wish.

At a press conference on January 11, 2017, President-elect Donald Trump explained for the first time how he would handle the many conflicts of interest that his business empire posed for his new role. His company, the Trump Organization, collected money from all over the world for luxury condos, hotel rentals, development projects, and club memberships, and he had made deals that put his name on everything from mail-order steaks to get-rich-quick courses. Could citizens trust him to put the common good ahead of personal profit? How would he assure Americans that payments to his business weren’t doubling as payoffs?

A journalist asked Trump if he would release his tax returns, as Presidents had done for decades. Trump said no, and then explained just how unconstrained he felt by such conventions. He’d recently learned that the President, being beholden only to the voters, is subject to none of the regulations that restrict subordinate officials from conducting private business on the side. He called the loophole “a no-conflict-of-interest provision,” as if it were a perk of his employment contract.

To illustrate just how glaring a conflict the law allowed him, Trump volunteered that, during the transition, he’d entertained a two-billion-dollar offer “to do a deal in Dubai.” The offer had come from Hussain Sajwani, an Emirati real-estate tycoon with close ties to his country’s rulers. Trump emphasized that he “didn’t have to turn it down.” Nevertheless, he’d passed, because he didn’t “want to take advantage of something”; he disliked “the way that looks.” Therefore, he continued, his eldest sons, Donald, Jr., and Eric, would assume daily management of his businesses until he left office.

Trump then turned things over to Sheri Dillon, one of his tax lawyers, who argued that he could hardly be expected to do more than the temporary handover. Trump would not “destroy the company he built.” Since Trump’s star turn on the NBC reality show “The Apprentice,” the Trump Organization had mainly sold the use of his name. Most of its profits came from developers who flew the Trump flag over buildings that he didn’t build or own, or from businesses that used his name to sell shirts, mattresses, or pizza. If Trump tried to off-load his whole company, Dillon explained, a buyer might overpay in order “to curry favor with the President,” or, just as worrisome, might demean the highest office in the land by crassly cashing in on the President’s name. Trump and his family, Dillon declared, would never do anything that might “be perceived to be exploitive of the office of the Presidency.”

That was a different era. Dillon’s firm stopped representing Trump in 2021, after the mob he stirred up attacked the U.S. Capitol. And in Trump’s second term the President and his family have paid no mind to their lawyer’s promise. During Trump’s first term, they pledged to abstain from any new deals overseas. That’s out the window. The Trumps are now cashing in on five major deals in the Persian Gulf alone. Donald, Jr., on a recent visit to Qatar, said that the family’s restraint during the first Trump Administration had not stopped his father’s critics from constantly accusing the family of “profiteering.” So the Trumps would no longer lock themselves in “a proverbial padded room, because it almost doesn’t matter—they’re going to hit you no matter what.” (A spokeswoman for the Trump Organization told me that it employs an outside ethics adviser—currently, Karina Lynch, a lawyer and a lobbyist who previously worked as a Republican Senate staffer and has represented Donald, Jr.—to “avoid even the appearance of impropriety.”)

Many payments now flowing to Trump, his wife, and his children and their spouses would be unimaginable without his Presidencies: a two-billion-dollar investment from a fund controlled by the Saudi crown prince; a luxury jet from the Emir of Qatar; profits from at least five different ventures peddling crypto; fees from an exclusive club stocked with Cabinet officials and named Executive Branch. Fred Wertheimer, the dean of ethics-reform advocates, told me that, “when it comes to using his public office to amass personal profits, Trump is a unicorn—no one else even comes close.” Yet the public has largely shrugged. In a recent article for the Times, Peter Baker, a White House correspondent, wrote that the Trumps “have done more to monetize the presidency than anyone who has ever occupied the White House.” But Baker noted that the brazenness of the Trump family’s “moneymaking schemes” appears to have made such transactions seem almost normal.

How much money does it all amount to? What’s the number? In March, Forbes, known for ranking the wealth of billionaires, estimated that Trump’s net worth had more than doubled in the previous year, surpassing five billion dollars. In July, the Times put Trump’s wealth at upward of ten billion. Yet both estimates included billions of dollars in paper profits that would almost certainly disintegrate if the Trumps pulled out of certain investments. (What’s Truth Social worth without him?) These estimates also included assets untainted by any obvious exploitation of the Presidency, such as properties that Trump owned before entering office, or fees paid by resort customers who simply want to play golf or book a hotel room.

Although the notion that Trump is making colossal sums off the Presidency has become commonplace, nobody could tell me how much he’s made. Norm Eisen, a government-ethics lawyer and a vocal Trump critic, said, “We don’t know the full amounts.” Robert Weissman, a co-president of the left-leaning advocacy group Public Citizen, said, “We will never really know.” Wertheimer noted that for decades Trump had boasted constantly, and in detail, about how rich he was. “He doesn’t talk about it anymore,” Wertheimer said. “He may be the greatest con artist in American history.”

A more considered accounting seemed in order. I decided to attempt to tally up just how much Trump and his immediate family have pocketed off his time in the White House.

In financial terms, the Presidency came to Trump at a fortuitous moment. Russ Buettner and Susanne Craig, the Times reporters who obtained some of Trump’s tax returns, conclude in their book, “Lucky Loser,” that by 2015 he had burned through much of the vast fortune passed on to him by his self-made father—an inheritance worth as much as half a billion dollars today. If Trump had put that money into the stock market, he could have ended up much richer. His life style also guzzled money. In 1990, in a deal to keep the Trump Organization out of bankruptcy, his lenders agreed that he needed four hundred and fifty thousand dollars a month just to make ends meet.

“The Apprentice,” on which he played the outsized version of himself that he has always tried to project to the world, once covered his losses. In the seven years following its début, in 2004, the show paid him $135.2 million. And its glamorizing effect allowed him to make money without buying or building anything, just by licensing his name and selling endorsements. Nearly all the real-estate projects he announced during this period—from Hawaii to Israel—were licensing deals. Licensing and endorsements made him $103.2 million in riskless profit. “I don’t want to say it was free revenue,” Donald, Jr., later testified in a New York court. But he did allow that the company’s licensing business was “a pretty spectacular system.”

Yet even the “Apprentice” windfall wasn’t always enough to keep Trump in the black. According to annual reports that the Trumps sent their lenders from 2011 to 2017, during those years Trump brought in $259 million from television and licensing contracts, but, thanks to his habit of overspending on properties, he still reported a negative cash flow of $46.8 million. Dwindling viewership numbers had killed “The Apprentice” in 2010, and by 2015 its doubly gimmicky offspring, “The Celebrity Apprentice,” was ailing, too. Trump’s licensing, endorsement, and “Apprentice” income fell to $22 million that year. Buettner and Craig note that between 2014 and 2016 Trump sold about $220 million in stock—nearly all his stock holdings—apparently to make up for losses as that income tapered off. Then, on June 16, 2015, Trump launched his first Presidential campaign with a speech in which he described Mexican immigrants as criminals and “rapists.” NBC kicked him off the air. Macy’s, Serta, and Phillips-Van Heusen ended endorsement deals.

After Trump won the election, lawsuits filed in the backlash against his Presidency added some big new expenses. By the start of his second term, he owed nearly five hundred million dollars to New York State, which had sued him for fraud, and more than $88 million to E. Jean Carroll, who had sued him for sexual assault and defamation. (Appeals are still pending.) Trump, in short, was in a tight spot when he first entered the White House and in an even tighter one when he returned. Just six months later, his financial situation has vastly improved.

Trump’s critics often describe his Administration as an oligarchy or a kleptocracy, conjuring parallels with Vladimir Putin. Yet experts who track international corruption told me that this is going too far. Global titans of self-dealing—such as Najib Razik, Malaysia’s former Prime Minister—divert vast sums from national coffers directly into their bank accounts. U.S. prosecutors have charged that Razik stole about four and a half billion dollars, including by transferring about seven hundred million into his personal accounts. Nobody has credibly accused Trump of simply embezzling payments to the I.R.S. Gary Kalman, the executive director at the U.S. branch of the corruption watchdog Transparency International, cautioned against “making stuff up just because everything is believable.”

Critics of Trump’s “oligarchy” invariably point to his relationship with Elon Musk. Musk contributed more than $290 million to back Trump and other Republicans in 2024. Trump then gave him an Administration role with seemingly extralegal power to reorder federal agencies; all the while, Musk’s businesses Tesla, SpaceX, and Starlink were profiting from government contracts or subsidies. In March, the President performed in what was effectively a television commercial on the White House lawn. Trump, after announcing that he would purchase a red Tesla parked there, declared, “It’s a great product—as good as it gets.” All that may be unseemly. Yet every American political campaign relies on private donations. All modern Presidents have sold access for campaign money, and all have rewarded donors with political appointments—especially ambassadorships.

More important, campaign-finance laws restrict how Trump can use his political war chest. Since reëntering the White House, Trump has raised the record-breaking sum of six hundred million dollars for his political operation. He can tap into that reserve to attack congressional enemies, and he can direct it toward other campaigns. (Donald, Jr., has contemplated a Presidential run.) Yet the money generally can’t bankroll personal expenses. In the campaign-money game, Trump plays at an Olympian level, but he hasn’t changed the rules.

Personal self-enrichment is where Trump is a true innovator, and his winnings in that category are also harder to quantify. On his tax returns, Trump has aggressively minimized the value of his assets and maximized the extent of his losses. On loan applications, he’s done the opposite, puffing up his wealth to borrow as much as possible. And on the financial-disclosure forms he’s been required to file as a candidate or as President, he usually provides only a business’s gross revenue, not its bottom line, thus reporting tens of millions of dollars in “income” from hotels that are actually losing money.

Bruce Dubinsky, a forensic accountant who testified in the fraud trial of Bernie Madoff and investigated the collapse of Lehman Brothers as a part of its bankruptcy, closely followed Trump’s New York fraud trial. Dubinsky told me that the opaque ownership structure of the Trump businesses makes it difficult to assess changes in his net worth. It’s similarly hard to isolate his Presidential profits, in part because estimating how much his businesses might have made if he weren’t President would require detailed comparisons with similar enterprises that have non-Presidential owners. By way of example, Dubinsky, who lives in Florida, noted that he’d recently visited the Trump golf course in Jupiter, “just to play golf.” He added, “So how much value to assign to his status as President is a daunting task.”

That blurriness is why ethics experts say that any outside business can pose a conflict of interest and may open a conduit for bribery. But, propriety aside, I was after a fair, dispassionate quantification of the Trumps’ profits from two Presidencies. Mar-a-Lago, the for-profit club that has become the MAGA mecca and the weekend White House, was an obvious place to start.

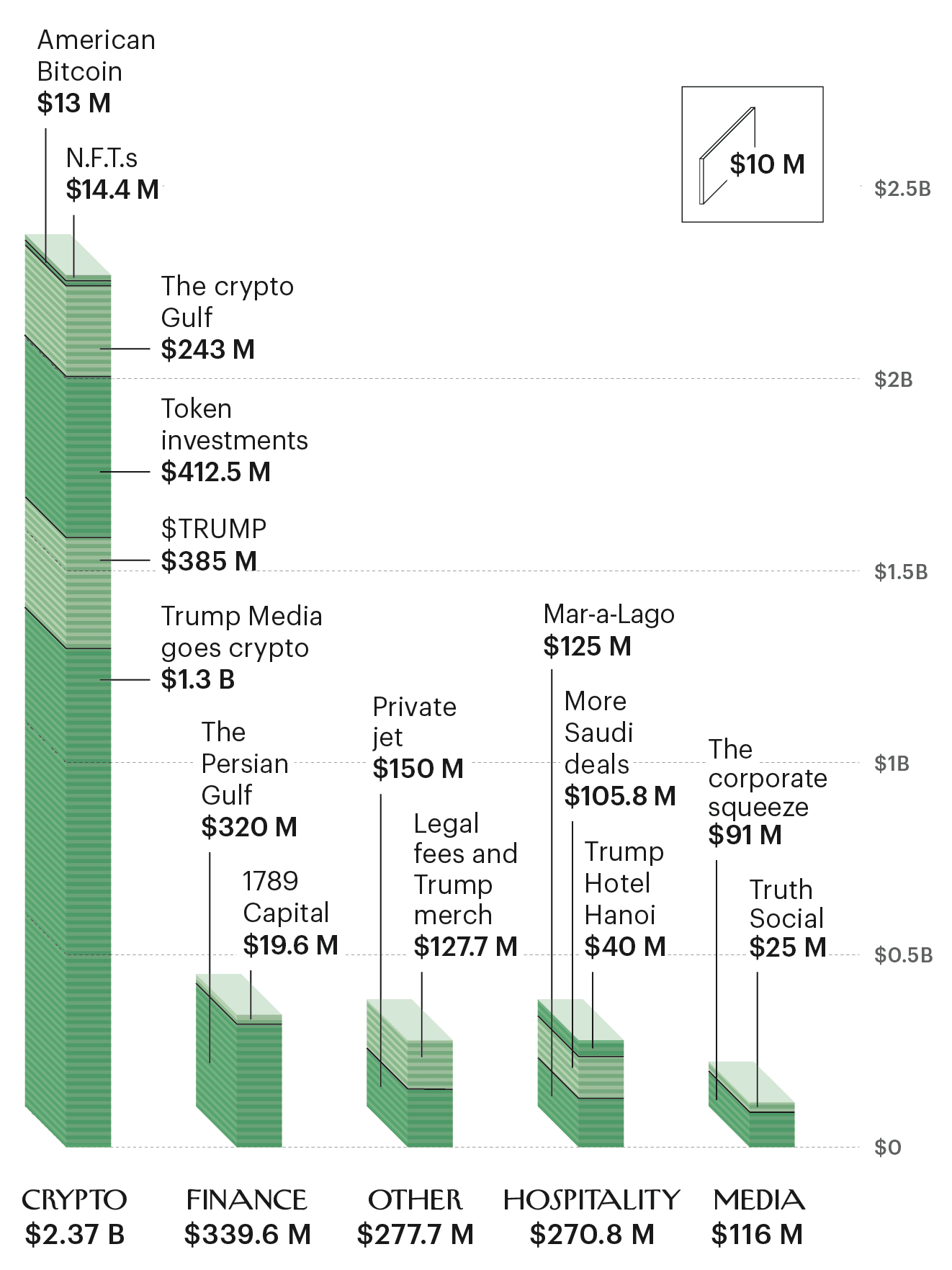

Chart by Francesco Muzzi

MAR-A-LAGO

In 2016, Trump, while running for President, was also suing a restaurateur for cutting ties over his bigoted comments about Mexican immigrants. In a deposition that summer, Trump testified that the Presidential race had so far had no “huge impact” on his hotel and resort businesses, which were “fairly steady.” One exception, he said, was Mar-a-Lago, the Palm Beach estate he’d turned into a private club after acquiring it, in 1985, for roughly ten million dollars. As though surprised by a happy accident, Trump testified that, according to the club’s manager, the campaign had given Mar-a-Lago “the best year we’ve ever had.”

If many Presidents have traded access for campaign donations, only Trump has run a business selling an open-ended opportunity to mingle with him and his circle. In addition to the revenue he generated by holding his own campaign events at his club, he has profited from other candidates, conservative groups, and influence seekers rushing to hold events there, too. The club says that it limits membership to five hundred people; each reportedly pays an annual fee of about twenty thousand dollars. But after the 2016 election Trump began jacking up the initiation fee. In 2016, it was a hundred thousand dollars; last fall, it was set to rise to a million.

Trump’s financial-disclosure forms indicate that since 2014 Mar-a-Lago’s annual revenue has jumped from ten million dollars to fifty million. At the same time, Forbes reported, operating costs have been stable, ranging from twelve million to sixteen million dollars a year. Adding it all up, I calculated that Trump’s Presidencies have brought him at least $125 million in extra profits from Mar-a-Lago.

Estimated gain: $125 million

LEGAL FEES AND TRUMP MERCH

Although candidates cannot pocket campaign contributions, no President has ever tried as hard as Trump to siphon off at least some of that money. According to the nonprofit OpenSecrets, in the past decade Trump’s campaigns have spent more than twenty million dollars at his own hotels and resorts, contributing to Mar-a-Lago’s spike in profits. But how much, if any, of this money reached his personal accounts is impossible to guess.

Trump’s 2016 and 2024 campaign operations paid him a total of eighteen million dollars for the use of his own Boeing 757—the so-called Trump Force One. (Air Force One ferried him around during the 2020 campaign, as is standard for a sitting President.) But Barack Obama, in 2008, and Mitt Romney, in 2012, each spent a comparable sum to charter campaign planes.

Trump, however, is the first Presidential candidate to run a private online store that competes against his own campaign in selling campaign-style merch, effectively diverting his supporters’ money into his own pocket. It’s as if a fashion designer had set up a table in front of a department store to sell knockoffs of his own company’s products, at the expense of its shareholders. Among the Trump Store’s wares: a red “Gulf of America” baseball hat (fifty dollars), a pair of Trump beer koozies (eighteen dollars), and Trump flip-flops (forty dollars). Buyers might well believe that such purchases fund the MAGA cause or its candidates, yet Trump’s financial-disclosure forms indicate that he has made more than seventeen million dollars in income from such sales. At those prices—with negligible marketing expenses, thanks to his role as head of state—that income is surely almost all profit. Trump’s most recent disclosure form also listed licensing income of $1.1 million from a Trump guitar, $2.8 million from Trump watches, $2.5 million from “sneakers and fragrances,” $3 million from an illustrated book called “Save America,” and $1.3 million from a “God Bless the USA” Bible. That adds up to at least $27.7 million from faux campaign paraphernalia.

A political campaign fund cannot pay a candidate’s personal legal bills. But Trump found a loophole: a campaign fund can be converted into a political-action committee, and the looser restrictions on a PAC allow the use of donor funds to pay such expenses. Through his PACs, Trump has spent more than a hundred million dollars of his supporters’ contributions to defend himself against an array of charges: that he defamed E. Jean Carroll while denying her account of his sexual assault, that he fraudulently hid a payoff to a porn star during the 2016 campaign, that he conspired to overturn the results of the 2020 election, and that he stole and hid classified documents after leaving the White House. Unless all those charges are part of a vast deep-state conspiracy, relieving Trump of the bills looks like a hundred-million-dollar gift for personal expenses.

Estimated gain: $127.7 million

Running total: $252.7 million

THE D.C. HOTEL

During the President’s first term, no business figured more prominently in Democratic allegations of corruption than did the Trump International Hotel in Washington. Zach Everson, who wrote an online newsletter about the scene there, told me that the hotel was “the epicenter of the swamp.” Foreign leaders booked blocks of rooms. Industry trade groups held conventions. Lobbyists, lawmakers, and Cabinet officials crowded the bar. Trump often visited; staff told Everson that tips suffered because guests stayed at their tables to gawk until the President left. If you wanted to curry his favor, where else in Washington would you stay? In 2018, when T-Mobile was seeking regulatory approval to acquire Sprint, John Legere, then T-Mobile’s chief executive, was spotted there. In ten months, he and other company executives spent nearly two hundred thousand dollars at the hotel; Legere denied any scheme to influence the White House and said he was a “longtime Trump-hotel stayer.” (The merger was approved.)

All this patronage surely flattered Trump’s ego, but it never fattened his wallet. The hotel lost money each year of his first term—a total of more than seventy million dollars. Industry executives familiar with the hotel’s operations told me that Trump’s Presidency repelled as many potential customers as it attracted. Many foreign leaders, lobbyists, and executives who might otherwise have paid handsomely for the Trump hotel’s location and luxury stayed elsewhere, fearing entanglement in an influence scandal. (T-Mobile’s Legere endured a grilling on Capitol Hill about his choice of accommodations.) In the two years after Trump’s election, hotels in Toronto, New York, Rio de Janeiro, and Panama City that had licensed the Trump name ditched it, presumably in part because it was driving away business. A Hawaii hotel followed suit in 2023.

Trump had agreed in 2012 to pay the federal government at least three million dollars a year for a long-term lease of the D.C. building, a former post-office headquarters, and to invest at least two hundred million in renovations. The hotel opened in 2016, and Trump sold it in 2022 for $375 million. Craig and Buettner, after reviewing his tax returns, conclude that he roughly broke even. Hilton Hotels took over the management, under its Waldorf Astoria brand, and people familiar with its operations said that its financial performance has improved markedly.

During Trump’s first term, Trump Turnberry, his golf resort in Scotland, also drew allegations of improper Presidential self-enrichment, because the U.S. military sometimes paid to put up service members there during overnight stops at the nearby Prestwick Airport. During the twenty-three months ending in July, 2019, the Pentagon spent at least a hundred and eighty-four thousand dollars at Trump Turnberry (at a discounted nightly room rate averaging $189.04).

Yet that property, too, lost money all four years of the first Trump Administration. It finally entered the black in 2022. And U.S. service members continued to stay there under President Joe Biden. An Air Force spokesman told me that there had been “no change” in the military’s use of the facility: “Aircrews are allowed to select the Trump Turnberry Resort, along with other hotel options in the area, if the lodging meets specific criteria of availability, suitability, expense, and proximity.”

Spending at Trump’s hotels by government agencies and influence seekers looked to me like a wash.

Estimated gain: $0

Running total: $252.7 million

THE PERSIAN GULF

The Persian Gulf has posed a unique commercial opportunity and ethical challenge for the first Commander-in-Chief who’s also a real-estate salesman. The Gulf’s Arab monarchs play complementary double roles: each is both a head of state and a major buyer of U.S. real estate and other assets. The Gulf royals put money in the very kinds of properties and investments that Trump’s family sells. In a recent interview with Tucker Carlson, Steve Witkoff, Trump’s Middle East envoy and a fellow real-estate mogul, expressed delight that the mind-set of Gulf rulers facilitates dealmaking: “Everybody’s a business guy there!” But these business guys were deeply entangled with the Trump crowd. Trump, Witkoff, and others in the two Trump Administrations—including Jared Kushner, the husband of Trump’s daughter Ivanka—had sold or tried to sell assets to the Gulf’s ruling families before entering government. And both sides can expect to do business again once Trump leaves office.

Unlike heads of state in, say, Western Europe, the Gulf monarchs wield extraordinary power over the businesses of their subjects. A Gulf monarch controls the fossil-fuel revenue that ultimately drives every enterprise in his country, from the lowliest shawarma stand to the finest resort. And he is unconstrained by independent courts or Western-style laws that might protect private interests. The richer a Gulf tycoon, the more he must depend on his sovereign’s good will. So a deal with a private firm is sometimes not much different from a deal with a ruler.

During the 2016 Republican primaries, Trump boasted of having sold condos to Saudis: “They buy apartments from me. They spend forty million, fifty million. Am I supposed to dislike them? I like them very much.” Nevertheless, he’d struggled to make licensing deals in the Gulf. The few developers outside North America willing to pay for the use of his family name were mostly building condominiums in lower-rent parts of the developing world. He’d made hundreds of thousands of dollars a year licensing his name for a two-tower project in Istanbul. (On his three most recent annual disclosure forms, he reported receiving $489,182, $392,360, and $288,061. Reporting periods can be irregular.) He’d also licensed his name for four apartment towers in India, six in South Korea, one in the Philippines, and another in Uruguay. (Resorts or other planned ventures in Georgia, Azerbaijan, and elsewhere fell through after he was elected.) Trump’s only beachhead in the Gulf was a deal with Hussain Sajwani, the tycoon close to Emirati rulers. In 2013, Sajwani, the self-styled “Donald of Dubai,” had agreed to pay the Trump Organization to manage a Trump-branded golf course, surrounded by villas, in Dubai.

When Trump was running for President in 2016, at least one emissary from the campaign suggested to the Emirati rulers that Trump’s deal with Sajwani gave them an in. Tom Barrack, Trump’s friend and informal adviser, wrote in an e-mail to the Emirati Ambassador, Yousef Al Otaiba, that Trump “has joint ventures in the U.A.E.!”

Barrack prompted the U.A.E. to begin courting Kushner, Trump’s incoming Middle East adviser, and this effort appeared to pay off stunningly. Through Kushner, the Emiratis helped persuade Trump to travel to the Persian Gulf for his first Presidential trip abroad. They also helped get Trump to support their preferred heir to the Saudi throne, Mohammed bin Salman, now the crown prince and de-facto ruler, instead of a royal cousin who’d long been the American favorite. Most remarkably, in 2017 Trump supported the U.A.E. and Saudi Arabia in a feud with neighboring Qatar. The Emiratis and the Saudis had accused their regional rival of supporting Islamist movements, and organized a blockade designed to starve the country. Qatar is a Pentagon partner, largely funding an American airbase west of Doha, and Trump’s stance contradicted the positions of his Secretaries of State and Defense. (The Saudis and the Emiratis patched things up with Qatar at the end of Trump’s first term; he and the rulers involved now act like the blockade never happened.)

Had the payments for the Dubai golf course helped the Emiratis win Trump’s favor? Would a deal with the Trump Organization have protected Qatar? A senior official of a Gulf state told me that the region’s rulers now view business with Trump “as a kind of safeguard.”

It did not take long after Trump’s first term for his family to return to the Gulf. He had left the White House in disgrace following the January 6, 2021, assault on the U.S. Capitol, but the scandal didn’t dislodge him from his position as a political kingmaker. Kevin McCarthy, the House Republican leader, had to make a pilgrimage to Mar-a-Lago to atone for declaring that Trump must accept responsibility for instigating the riot. Yet Trump and his family were now liberated from the duties of public office, and freer than ever to cash in on his status as the once and future President.

Kushner went first. During Trump’s first term, he’d quietly backed Mohammed bin Salman during the prince’s consolidation of power in Riyadh, even pushing Trump to stand by him after Saudi agents murdered Jamal Khashoggi, a Washington Post columnist and a Virginia resident. Shortly after leaving the White House, Kushner asked the Saudi sovereign wealth fund to invest two billion dollars with a private-equity firm that he was founding, Affinity Partners.

The Saudi fund’s panel of investment advisers unanimously objected. Kushner had worked almost exclusively in real estate and never in private equity, and he was asking the Saudis to put up a vast sum when no American had invested a penny. The panel called the management fee that Kushner wanted—1.25 per cent of the firm’s assets, or $25 million, each year—“excessive,” given his lack of relevant experience. The advisers also worried about a “public relations” problem: the deal might look like a payoff.

The Saudi fund’s board, controlled by the crown prince, ignored the advice. Two billion dollars it was. Emirati and Qatari investors soon kicked in hundreds of millions more. Terry Gou, the Taiwanese businessman and politician who founded the manufacturing giant Foxconn and maintains close ties to China’s leaders, also invested. (While in the White House, Kushner helped arrange subsidies for a Foxconn factory in Wisconsin.) And in 2024, as Trump was poised to retake the Presidency, Kushner’s firm raised an additional $1.5 billion from the Qataris and Emiratis, bringing its assets under management to $4.8 billion.

If all the investors besides the Saudis pay the industry-standard management fee of two per cent a year, Affinity’s annual revenue comes to $81 million. Under conventional private-equity terms, Kushner’s firm, after repaying management fees, can keep an additional twenty per cent of any returns on its investments (although Kushner agreed to share some of that with the Saudis). That cut of the profits is typically the biggest windfall for a private-equity firm, and reports indicate that at least some of Kushner’s early investments, including in an Israeli financial firm and a German fitness company, are paying off. But even if Kushner fails utterly—a renewable-energy lender that his fund invested in, Solar Mosaic, recently filed for bankruptcy, in part because of Trump policy changes—Affinity still stands to take in $810 million over ten years, a typical life span for such a fund.

Congressional Democrats have asked if Kushner might be selling influence as part of the deal. Since leaving the Trump Administration, Kushner has described himself as an informal foreign-policy adviser to his father-in-law and to members of Congress. He’s also reportedly conversed with the Saudi crown prince about such foreign-policy matters as relations with Israel, and at a conference last year he said that, thanks to his White House experience, he and his firm could “do things on the geopolitical side, on the connections side.”

Last fall, Senator Ron Wyden, of Oregon, and Representative Jamie Raskin, of Maryland, unsuccessfully urged the Biden Administration’s Department of Justice to appoint a special counsel to investigate whether Kushner was illegally acting as an unregistered foreign agent. In a public letter, Wyden and Raskin argued that “the Saudi government’s decision to engage Affinity for investment advice” appeared to be “a fig leaf for funneling money directly to Mr. Kushner and his wife, Ivanka Trump,” possibly “to curry favor” or “reward them for favorable U.S. policy towards Saudi Arabia during the first Trump administration.” (Kushner called the letter a political stunt, and has argued that critical coverage of the Saudi deal only helps his firm. Although journalists “think they’re writing a bad thing,” he told Forbes, businesspeople who read those articles discover “that I’m very trusted by my partners.”)

Affinity’s fees, of course, must cover overhead, from staff compensation to office space. But Kushner is the founder and sole owner, and it’s unimaginable that the firm could have reaped such sums from those investors without his father-in-law’s Presidencies. We might conservatively assume that he personally keeps between half and two-thirds of Affinity’s fees over ten years. (He will make far more if the fund turns a profit.) Half would be $405 million. On Wall Street, the “present value” of that stream of future income—taking into account the cost of delay—is about $320 million.

Kushner also has real-estate projects in the works that pose additional conflicts of interest for Trump. A partnership with the Serbian government (backed by an Emirati investor) to build a Trump-branded hotel in Belgrade has been derailed by the discovery that its approval was based on a document that a Serbian official allegedly forged. But in January the Albanian government preliminarily approved a partnership with Kushner to build a hundred-and-eleven-acre resort on one of the few undeveloped islands in the Mediterranean. The project is said to entail a $1.4-billion investment. Still, both are real-estate developments—Kushner’s area of expertise. Unlike with the Saudi investment, it’s unfair to attribute those deals entirely to Trump’s public office, and it’s premature to guess what Kushner or his investors in the projects might someday earn. It is safest to say only that his private-equity firm has added at least $320 million to the family’s Presidential profits.

Estimated gain: $320 million

Running total: $572.7 million

MORE SAUDI DEALS

Trump’s first business with the Saudis upon leaving the White House involved golf. After the Capitol riot, the P.G.A. of America cancelled a contract to hold its televised championship the next year at his course in Bedminster, New Jersey, depriving Trump of valuable publicity. Fortunately for him, Saudi Arabia was launching its own pro-golf association,

THE PRIVATE JET

In May, the President returned from formal state visits to Saudi Arabia, the U.A.E., and Qatar with his most unusual deal so far, one without any pretense of a sale. He announced that the Emir of Qatar had agreed to make a “free gift” of a royal Boeing 747-8 for Trump’s use as a flashy Presidential jet. Trump characterized the transfer as a boon for American taxpayers: the Air Force would retain ownership of the plane until he left office. Yet Trump also said that the Pentagon would then pass the jet to his Presidential-library foundation. This “free gift” looked enough like a personal favor that the Emir has requested a memorandum of understanding confirming that it’s a donation from one government to another, in order to protect him from allegations of bribery. He also wants it in writing that Qatar didn’t propose the handover, and made it only at the President’s request. (A Qatari official told me that negotiations are ongoing.)

TRUMP HOTEL HANOI

In September, 2024, with polls forecasting Trump’s likely return to office, Tô Lâm, the General Secretary of Vietnam’s ruling Communist Party, visited New York and dispatched a Central Committee member to wrap up a Trump resort deal. The Central Committee member oversaw the signing of an agreement between the Party committee of Hung Yen Province and a consortium of investors arranged by the Trump Organization. The same day, Trump took time away from the campaign to join Eric in signing an agreement with a Vietnamese company, known for its office parks, that will build the property and pay the Trumps for the use of their name. The planned development, with a projected cost of $1.5 billion, will include a hotel, residences, and fifty-four holes of golf, occupying an area three times the size of Central Park. It appears to be the largest Trump-branded development in the world.

THE CORPORATE SQUEEZE

In a 2016 law-review article, Susan Seager, a First Amendment lawyer and a professor at the University of California, Irvine School of Law, described Trump as a “libel loser.” In the past five decades, he has lost or withdrawn a dozen suits against media companies, and failed to follow through on many other threats. The handful of claims that he filed after leaving the White House all seemed certain to end similarly. Last spring, for example, he sued ABC News for defamation because its anchor George Stephanopoulos said that a court had found Trump “liable for rape.” The court had found Trump liable for sexually abusing and defaming E. Jean Carroll, and the judge had emphasized that Carroll had

TRUTH SOCIAL

In October, 2021, Trump announced a plan to launch his own social-media platform, Truth Social. The social-media market was crowded. Yet Trump, who had formed a shell company for the platform, said that he had already agreed to a lucrative merger. His shell company was combining with Digital World Acquisition Corp., a financial contrivance called a special-purpose acquisition company.

1789 CAPITAL

On January 31st, Ned’s Club, a chain of luxury social clubs with locations in London, New York, and Doha, opened an outpost near the White House. Ned’s is owned by the investor Ronald Burkle, a Democratic donor, who is also the chairman and majority shareholder in Soho House, a kind of sister company. The Washington Ned’s is a joint venture with Michael Milken, the financier who was convicted in 1990 of securities fraud and pardoned in 2020 by Trump. Kellyanne Conway, the former Trump adviser, sits on the club’s membership committee. Commerce Secretary Howard Lutnick, Treasury Secretary Scott Bessent, and former Treasury Secretary Steven Mnuchin have reportedly been seen there.

CRYPTO

Eric Trump, the public face of the Trump Organization while his father is in office, often says that his family first “fell in love with crypto” in the years after the Capitol riot. Big banks dropped the Trumps—including Deutsche Bank, their most important lender, and Capital One, where the Trump Organization had hundreds of accounts. At a recent crypto conference, Eric framed this blackballing, as he often does, as an example of bias against “a political view that might not have been popular with some of the big financial institutions.” He also described his family’s embrace of digital finance as a form of revenge: “The banks made the biggest mistake of their lives.”

TOKEN INVESTMENTS

Trump collected some of his N.F.T. fees in the form of digital currency, giving him his first incentive to start talking it up. In December, 2023, Arkham, a research firm, reported that a digital wallet linked to Trump held about four million dollars’ worth of crypto. On his most recent disclosure form, Trump reported that his digital wallet contained at least a million dollars’ worth of crypto.

THE CRYPTO GULF

In March, World Liberty announced that it would sell a type of cryptocurrency known as stablecoin. Unlike buying bitcoin or other digital assets, purchasing stablecoin is supposed to resemble putting money into a checking account. A buyer can pass them to other digital wallets the way you might transfer money from one checking account to another; an owner of stablecoin should always be able to redeem them for dollars, at a constant value. Until July, stablecoins were largely unregulated, and the best known have become a mainstay of money laundering; some issuers, meanwhile, have diverted supposedly secure deposits into crypto Ponzi schemes.

AMERICAN BITCOIN

The origins of the Trump family’s third crypto business date back about five years, to when Donald, Jr., and Eric got to know Kyle Wool, a stockbroker who had recently left Morgan Stanley. Wool wore his hair in the slicked-back style of Michael Douglas in “Wall Street” and golfed at the Trump club in Jupiter. At the time, he oversaw wealth management at an obscure brokerage, Revere Securities. (Morgan Stanley paid fifty thousand dollars to settle a lawsuit claiming that Wool had made unauthorized trades with a client’s money—one of several similar allegations he has faced. He has denied any wrongdoing.)

TRUMP MEDIA GOES CRYPTO

The family’s fourth crypto venture is an attempt by Trump Media & Technology Group to reinvent itself. In April, the company capitalized on the new Administration’s crypto-friendly policies by announcing a plan to sell volatile crypto assets to ordinary investors. The technical difficulty of buying crypto has long deterred most small and unsophisticated investors. But, under Trump, the S.E.C. has made it much easier for investment companies to sell crypto to anyone with a standard brokerage account, through shares in what are known as exchange-traded funds, or E.T.F.s, that track the price of bitcoin, Ethereum, or other digital assets. The policy change represents a giant advance for the crypto industry. Trump Media jumped on the bandwagon, making plans to sell Trump-branded E.T.F.s, which will trade on the New York Stock Exchange. To do so, the company formed a partnership with Crypto.com, a Singapore-based exchange that was fighting an S.E.C. enforcement action for violating the agency’s regulations. Crypto.com had sought to win Trump’s favor by donating a million dollars to his Inauguration; a few days after its deal with Trump Media, it announced that the S.E.C.’s investigation had ended.

$TRUMP

Three days before his second Inauguration, Trump launched the fifth of his family’s crypto vehicles: selling $TRUMP, a digital token. $TRUMP doesn’t purport to hold value in the way that bitcoin or stablecoins do. Nor does $TRUMP entitle a buyer to a vote on a company’s future direction, as World Liberty’s initial token does. It does not even convey the right to own a digital cartoon of Trump. It’s a meme coin, a novelty, a bit of fun—the fun, for those who enjoy it, of paying Donald Trump. Eight years after his lawyer promised that his family would never exploit the Presidency for profit, Trump had distilled that exploitation to its purest possible form.

DINNER AND DESSERT

During the dinner, I stood outside the Trump National Golf Club in Sterling, Virginia, trying to glimpse some of the buyers hoping to whisper in the President’s ear. Dozens of protesters held banners reading “Stop Trump’s Crypto Corruption” and “America Is Not for Sale.” Senator Jeff Merkley, an Oregon Democrat who has introduced a bill that would bar senior officials from selling meme coins or stablecoins, addressed the crowd, calling the dinner “the Mt. Everest of corruption.”

Unfettered greed